The global wind turbine bearing market plays a foundational role in the performance, durability, and efficiency of modern wind energy systems. As global wind power capacity continues to expand, demand for high-performance bearings capable of withstanding extreme loads, fluctuating speeds, and harsh environmental conditions has accelerated significantly. Bearings are mission-critical components within wind turbines, ensuring smooth rotational movement, minimizing frictional losses, and supporting substantial structural and dynamic loads across turbine assemblies.

According to Research Intelo, the global wind turbine bearing market was valued at USD 9.8 billion in 2024 and is projected to reach USD 22.1 billion by 2033, expanding at a robust CAGR of 9.5% during the forecast period. This strong growth trajectory reflects increasing onshore and offshore wind installations, the scaling of turbine capacities beyond 10–15 MW, and rising emphasis on operational efficiency and lifecycle optimization.

Market Overview

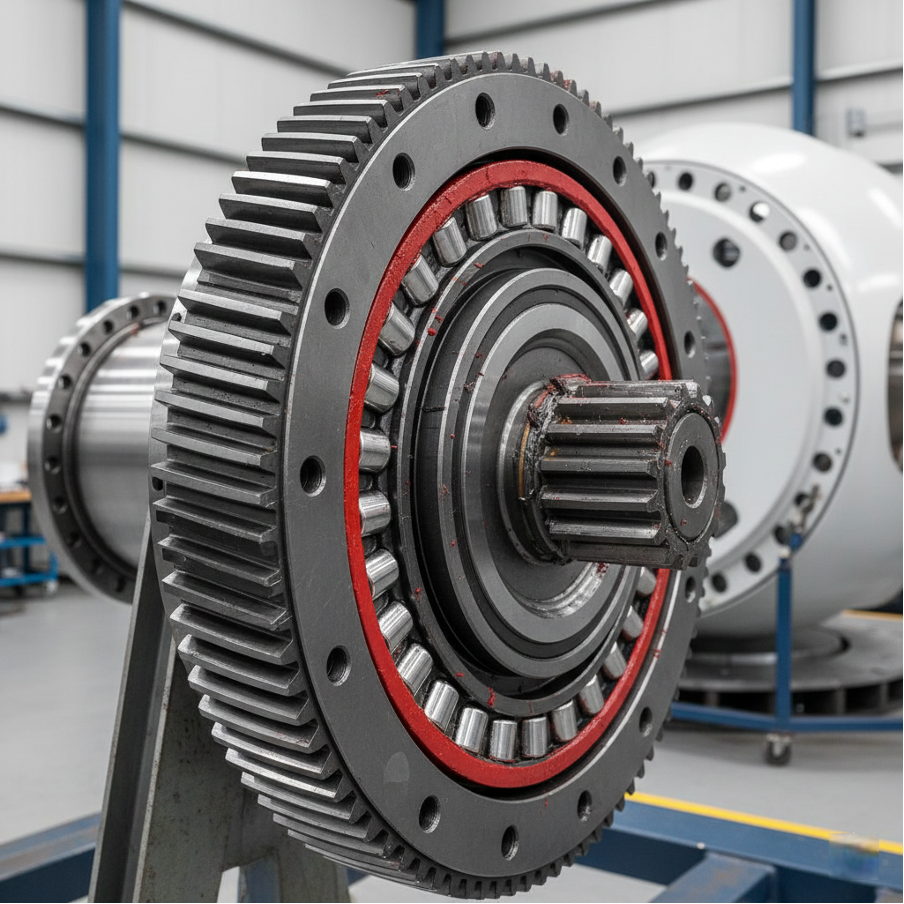

Wind turbine bearings are highly engineered mechanical components designed to operate under high axial and radial loads, continuous rotational stress, and challenging environmental conditions such as temperature variations, humidity, and salt exposure. These bearings are deployed across multiple critical subsystems, including:

- Main shaft assemblies

- Gearboxes

- Generators

- Pitch systems

- Yaw systems

The increasing size of wind turbines, particularly offshore units exceeding 12 MW, has intensified performance requirements for bearings. Larger rotor diameters generate higher torque loads, requiring enhanced load distribution, superior fatigue resistance, and longer service intervals. Manufacturers are focusing on advanced metallurgy, precision engineering, optimized internal geometries, and surface treatment technologies to meet evolving industry standards.

In addition, lifecycle cost reduction has become a central industry priority. Bearing reliability directly influences turbine uptime, maintenance scheduling, and overall project profitability.

Key Market Drivers

1. Technological Innovation and Automation Trends:

The shift toward larger and more powerful wind turbines, particularly in offshore applications, has necessitated significant advancements in bearing design. Bearings must now withstand higher dynamic loads, extended maintenance intervals, and extreme weather conditions. Key technological improvements include advanced high-strength alloy steels with improved fatigue resistance, hybrid ceramic rolling elements to reduce friction and wear, enhanced lubrication systems with extended service life, integrated smart sensors for real-time condition monitoring. The integration of predictive maintenance systems enables early fault detection through vibration and temperature analytics. This reduces unplanned downtime and significantly extends operational lifespan.

2. Growing Demand for Reliable and High-efficiency Turbines:

As utilities, independent power producers, and corporations increase renewable energy procurement, emphasis has shifted toward total cost of ownership (TCO) optimization. Reliability, reduced maintenance frequency, and higher energy output have become central performance metrics. High-performance bearings contribute to improved drivetrain efficiency, lower frictional losses, reduced failure rates, enhanced gearbox and generator longevity

The growing deployment of direct-drive turbines, which eliminate gearboxes but require large-diameter main bearings, is further reshaping product demand dynamics within the market.

3. Regulatory Support, Policy Reforms, and Financial Incentives:

Governments worldwide are implementing renewable portfolio standards, production tax credits, feed-in tariffs, and competitive auction mechanisms to accelerate wind energy deployment. These policies reduce financial risk for developers and encourage large-scale installations.

Stringent carbon reduction mandates and net-zero commitments are compelling energy providers to expand wind capacity rapidly. As turbine installations grow, demand for durable, high-load bearings continues to rise correspondingly.

4. Global Shift Toward Renewable Energy and Decarbonization:

The accelerating global transition toward renewable energy sources, particularly wind power, has significantly strengthened long-term market fundamentals. Nations striving to achieve carbon neutrality and energy security are expanding both onshore and offshore wind infrastructure.

Wind turbine bearings are essential to ensuring turbine reliability, operational stability, and performance efficiency. As cumulative installed wind capacity increases globally, both new installations and replacement demand from aging fleets are supporting sustained market expansion.

Market Segmentation

The wind turbine bearing market can be segmented based on bearing type, turbine type, installation location, and application.

By Bearing Type

- Main shaft bearings

- Gearbox bearings

- Generator bearings

- Pitch and yaw bearings

Main shaft bearings represent a critical segment due to their responsibility for supporting rotor loads and transferring torque. As turbine sizes increase, demand for large-diameter spherical and tapered roller bearings is rising significantly.

Gearbox bearings also hold a substantial market share, particularly in geared turbine configurations, where multiple bearing sets manage torque multiplication and rotational alignment.

By Turbine Type

- Horizontal axis wind turbines (HAWT)

- Vertical axis wind turbines (VAWT)

Horizontal axis turbines dominate global installations due to higher efficiency and scalability for utility-scale projects. Consequently, bearing demand remains heavily concentrated within HAWT configurations.

By Installation Location

- Onshore

- Offshore

Onshore installations account for the larger revenue share due to established infrastructure and lower capital expenditure requirements. However, offshore installations are projected to witness faster growth, driven by higher turbine capacities and strong wind resource availability in marine environments.

Offshore applications require specialized bearings with enhanced corrosion resistance, sealing mechanisms, and extended lubrication performance.

Regional Insights

- Europe holds the largest share of the market, accounting for approximately 38% of total market value in 2024. The region’s mature wind energy ecosystem, combined with strong offshore deployment in countries such as Germany, Denmark, and the United Kingdom, underpins its leadership position. Aggressive renewable energy targets, technological innovation, and sustained infrastructure investments continue to reinforce regional dominance, particularly in offshore wind.

- Asia Pacific represents the fastest-growing regional market, projected to expand at a CAGR of 11.8% from 2024 to 2033. China remains the largest contributor, supported by extensive domestic manufacturing capabilities and large-scale wind farm deployments. India, Japan, and South Korea are also accelerating wind installations due to rising energy demand, urbanization, and supportive government initiatives. Expansion of offshore wind projects in China and South Korea is further driving demand for high-capacity bearings.

- Latin America, Middle East, and Africa regions represent emerging growth markets. Countries such as Brazil and South Africa are expanding wind infrastructure through international partnerships and foreign direct investments. However, regulatory uncertainties, infrastructure gaps, and higher upfront capital costs present structural challenges. Over time, improving policy clarity and technology transfer are expected to support gradual adoption.

Competitive Landscape

The wind turbine bearing market is moderately consolidated, with global bearing manufacturers and specialized industrial suppliers competing on innovation, durability, and customization capabilities.

Key competitive strategies include:

- Strategic partnerships with wind turbine OEMs

- Long-term supply agreements

- Expansion of localized manufacturing facilities

- Investment in advanced R&D centers

- Vertical integration across the value chain

The aftermarket segment is gaining importance as aging wind fleets require refurbishment and replacement bearings. Lifecycle service contracts and predictive maintenance solutions are emerging as high-margin revenue streams.

Localization strategies are increasingly adopted to mitigate supply chain risks and reduce lead times.

Technological Innovations

Several advancements are shaping the next phase of market evolution:

- Advanced Materials: Development of ultra-clean steels and hybrid ceramic bearings to enhance fatigue life.

- Improved Lubrication Systems: Automated lubrication units and long-life synthetic greases reduce maintenance intervals.

- Surface Engineering: Anti-corrosion coatings and plasma treatments improve performance in offshore environments.

- Smart Bearings: IoT-enabled sensors provide real-time vibration, load, and temperature data for predictive analytics.

- Digital Twins: Simulation-based monitoring improves failure forecasting and asset optimization.

These innovations collectively improve operational reliability while reducing lifecycle costs.

Challenges

Despite strong growth prospects, the market faces several constraints:

- Volatility in steel and specialty alloy prices

- High precision manufacturing requirements

- Installation complexity in offshore environments

- Standardization gaps for next-generation bearing technologies

- Regulatory uncertainties in emerging markets

Addressing these challenges requires coordinated efforts across material suppliers, OEMs, regulatory bodies, and service providers.

Future Outlook

The wind turbine bearing market is poised for sustained expansion through 2033. With market value projected to grow from USD 9.8 billion in 2024 to USD 22.1 billion by 2033, technological advancement and renewable energy expansion will remain primary growth engines.

Increasing turbine capacities, rapid offshore deployment, and digitalization of maintenance systems will continue reshaping demand dynamics. Simultaneously, rising replacement demand from aging wind fleets will provide additional revenue stability.

Long-term industry evolution will be defined by advanced material science, smart monitoring integration, supply chain resilience, and continuous innovation in bearing design. As wind energy becomes central to global decarbonization strategies, high-performance wind turbine bearings will remain indispensable in ensuring efficiency, reliability, and long-term energy sustainability.